Your Taxes and Obamacare

I have addressed certain components of the Affordable Care Act in previous posts alerting readers to some of the highly discriminating new taxes targeting high earners, which were originally given no press or debate, but are a part of the Act and only impact a small minority of taxpayers at large.

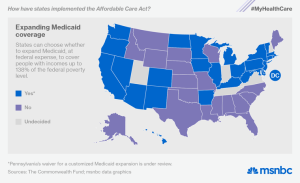

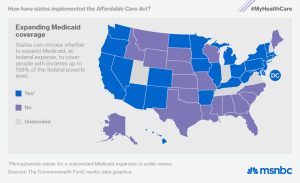

As a graphic for this article I included a national map of states accepting Federal money increasing the scope of our historical coverage for low wage earners; Medicaid. If a taxpayer has a Tax Home in one of the states accepting the enhanced Federal funds, the taxpayer may have applied for coverage under the ACA or Obama Care, but the taxpayer may wind-up with coverage back in Medicaid.

However with this Blog entry we are now discussing how Your Taxes and the Affordable Care Act will impact every taxpayer’s 1040 (and state Medicaid roles), and undoubtedly cause many last minute filers to scramble with a lot of frantic reading, resulting in some frustration.

Starting with this year’s filing season, taxpayers must report certain information related to health care coverage on their 2014 tax return when they file this April. In addition, taxpayers must provide proof of health insurance coverage or that they have received an exemption.

With that in mind, let’s take a look at how the Affordable Care Act might affect your tax situation, and based on your type of coverage, which new tax forms you might be receiving.

Tip: For additional information about IRS tax forms related to health care insurance, please see the article, Health Care Law: Changes to IRS Tax Forms, below.

Overview

The biggest change for most taxpayers is found on Line 61 of Form 1040, where individuals must either check a box to show they had health insurance or pay a penalty. In general, the penalty applies to individuals who did not have health insurance for more than three months in 2014.

In 2014, the penalty is the greater of one percent of modified adjusted gross income or $95 per adult ($47.50 per child under age 18, up to a maximum of $285 per family). While the IRS cannot issue a lien against you in order to make you pay the penalty, they are allowed to withhold the money from your refund.

Certain persons may qualify for an exemption from the penalty such as those who do not need to file a tax return ($10,150 for individuals, $13,050 for heads of household, and $20,300 for a married couples filing jointly). Other exceptions (there are eight in total and then a loss of hardship exemptions as well) include being a member of a federally recognized tribe or qualifying for a hardship exemption if you filed for bankruptcy in the last 6 months or had medical expenses you couldn’t pay in the last 24 months that resulted in substantial debt.

The Exemptions are as follows: (from https://www.healthcare.gov/fees-exemptions/exemptions-from-the-fee/ & https://www.healthcare.gov/fees-exemptions/hardship-exemptions/)

- You’re uninsured for less than 3 months of the year

- The lowest-priced coverage available to you would cost more than 8% of your household income

- You don’t have to file a tax return because your income is too low (Learn about the filing limit (PDF))

- You’re a member of a federally recognized tribeor eligible for services through an Indian Health Services provider

- You’re a member of a recognized health care sharing ministry

- You’re a member of a recognized religious sect with religious objections to insurance, including Social Security and Medicare

- You’re incarcerated (either detained or jailed), and not being held pending disposition of charges

- You’re not lawfully presentin the U.S.

- You qualify for a hardship exemption.

- You were homeless

- You were evicted in the past 6 months or were facing eviction or foreclosure

- You received a shut-off notice from a utility company

- You recently experienced domestic violence

- You recently experienced the death of a close family member

- You experienced a fire, flood, or other natural or human-caused disaster that caused substantial damage to your property

- You filed for bankruptcy in the last 6 months

- You had medical expenses you couldn’t pay in the last 24 months that resulted in substantial debt

- You experienced unexpected increases in necessary expenses due to caring for an ill, disabled, or aging family member

- You expect to claim a child as a tax dependent who’s been denied coverage in Medicaid and CHIP, and another person is required by court order to give medical support to the child. In this case, you don’t have the pay the penalty for the child.

- As a result of an eligibility appeals decision, you’re eligible for enrollment in a qualified health plan (QHP) through the Marketplace, lower costs on your monthly premiums, or cost-sharing reductions for a time period when you weren’t enrolled in a QHP through the Marketplace

- You were determined ineligible for Medicaid because your state didn’t expand eligibility for Medicaid under the Affordable Care Act

- Your individual insurance plan was cancelled and you believe other Marketplace plans are unaffordable

- You experienced another hardship in obtaining health insurance

Caution: Taxpayers who believe they qualify for an exemption must apply and receive an exemption certificate from the Marketplace.

There’s an additional twist for the approximately eight million people who purchased health insurance through the Healthcare Marketplace (“the Exchanges”), many of whom received subsidies that were paid to insurance companies and applied directly to their insurance premiums.

What taxpayers might not realize is that in many cases these subsidies were based on household size and income for 2012. Remember, the enrollment period began October 1, 2013 before taxpayers had filed their 2013 tax returns.

If income or household size changed in 2014 and the IRS was not notified of these updates, taxpayers may be liable for paying additional subsidy monies or conversely, receive refunds for amounts overpaid. In other words, if you received a bonus in 2014 (change in household income), it could mean that you owe the government money.

Enrollment through an Employer, Private Insurance, Medicaid or Medicare

New Tax Forms: 1095-B, 1095-C

1095-B. If your healthcare coverage is provided by private insurers or self-funded plans, you should receive Form 1095-B; however, because tax year 2014 is a transition year, these forms are not required when filing your 2014 tax return.

1095-C. If your healthcare coverage is provided by your employer, you should receive Form 1095-C; however, because tax year 2014 is a transition year, these forms are not required when filing your 2014 tax return.

Enrollment through the Healthcare Marketplace

New Tax Forms: 1095-A, Form 8962

Form 1095-A. If you purchased health insurance from the Marketplace you will receive Form 1095-A showing details of your coverage such as the effective date, amount of your premium payment, and any advanced premium credit you received.

Form 8962. The amount of any advanced premium credit you received in 2014 is reported on Form 8962. This form is also used to figure out the actual premium credit as well.

No Health Insurance

If you DO qualify for an exemption: Taxpayers must apply for the exemption from the Marketplace and if approved, will receive an exemption certificate number, which must be reported on Form 8965.

If you DO NOT qualify for an exemption: Taxpayers that do not qualify for an exemption and are uninsured are required to pay a penalty (see above) when filing their tax return. Form 8965 is used to calculate the penalty.

Don’t hesitate to call or email with any questions about the ACA and your taxes.